Co-designing clouds for the data future of fintech : the next generation of StockPrice infrastructure

We first discussed the emergence of “big data”, and its impact on computing and storage needs, with Associate Professor Paul Lajbcygier and his team in 2014. The Research Cloud at Monash initial engagement enabled the “Stock Price Impact Models Study” to get off the ground with immediate high-impact research output. A few months later, in 2015, we’ve showcased their incremental update to the study “Stock Price Impact Models Study on R@CMon Phase 2 (Update)”, which produced another high-impact publication. Then in 2018, Associate Professor Paul Lajbcygier and Senior Lecturer Huu Nhan Duong held the “Monash workshop on financial markets” at the Monash University, attracting highly prominent Australian and international researchers to talk about topics such as “market design and quality”; “high frequency trading”; “volatility and liquidity modelling”; and many more.

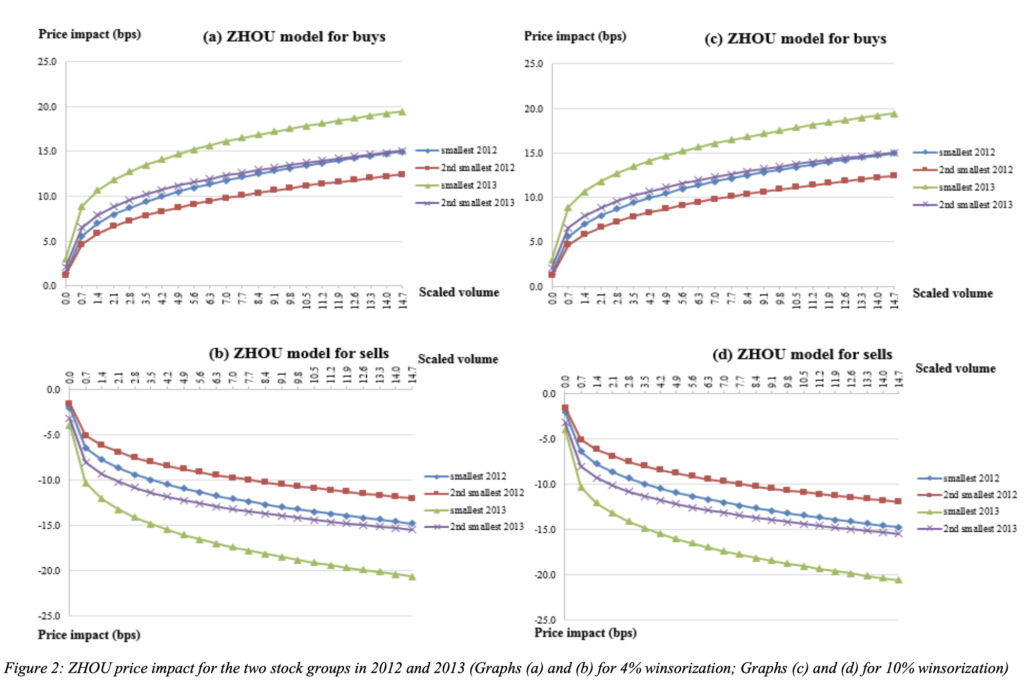

Pham, Manh Cuong and Duong, Huu Nhan and Lajbcygier, Paul, A Comparison of the Forecasting Ability of Immediate Price Impact Models (September 18, 2015). Available at SSRN: https://ssrn.com/abstract=2515667 or http://dx.doi.org/10.2139/ssrn.2515667

Fast forward to 2020 and despite the current world and local circumstances, Paul and his team continue to excel in producing more high impact research outcomes. Their recent successes include a “Journal of Economic Dynamics and Control” publication entitled “The effects of trade size and market depth on immediate price impact in a limit order book market” and an Interfaculty Seeding Grant with the Monash Business School and Faculty of Information Technology to study high frequency trading using machine learning methodologies. There are also numerous research outputs to be submitted towards the end of 2020 and many more towards Q1 of 2021. This surge in high impact outputs correlates to a recent optimisation in the way big queries are executed on the memory engine of the underlying R@CMon-hosted database.

The speed up compared to previous data runs is around four times. This means we can now use more of the memory in the big memory machine effectively.

Paul Lajbcygier, Associate Professor, Banking & Finance, Monash Data Futures Institute

The R@CMon team are currently preparing for the next round of cloud resources uplift in 2021 where “persistent memory” (e.g Intel Optane DC) components are being considered to be included in the resource pool (flavours) available to research cloud users. This could provide even more substantial speedups to big queries on stock price big data. Once ready, the R@CMon team will engage Paul’s team again to utilise these resources.

This article can also be found, published created commons

- Revote, Jerico; Quenette, Steve; Aung, Swe Win (2021): Co-designing clouds for the data future of fintech. Monash University. Online resource. https://doi.org/10.26180/13571279.v2.